Have you ever picked up a generic prescription and been shocked by the price? You check your insurance card, think you’re covered, and then the pharmacist says, "That’ll be $45." But a few blocks away, the same drug costs $4 cash. This isn’t a mistake. It’s how the system was built.

Who’s really setting the price?

When you think about who controls the price of your generic pills, you probably imagine your doctor, your insurer, or the pharmacy. But the real power lies with Pharmacy Benefit Managers, or PBMs. These are the hidden middlemen between your insurance company and the pharmacy where you fill your prescription. PBMs don’t sell drugs. They don’t make them. But they decide how much pharmacies get paid-and how much you pay out of pocket.

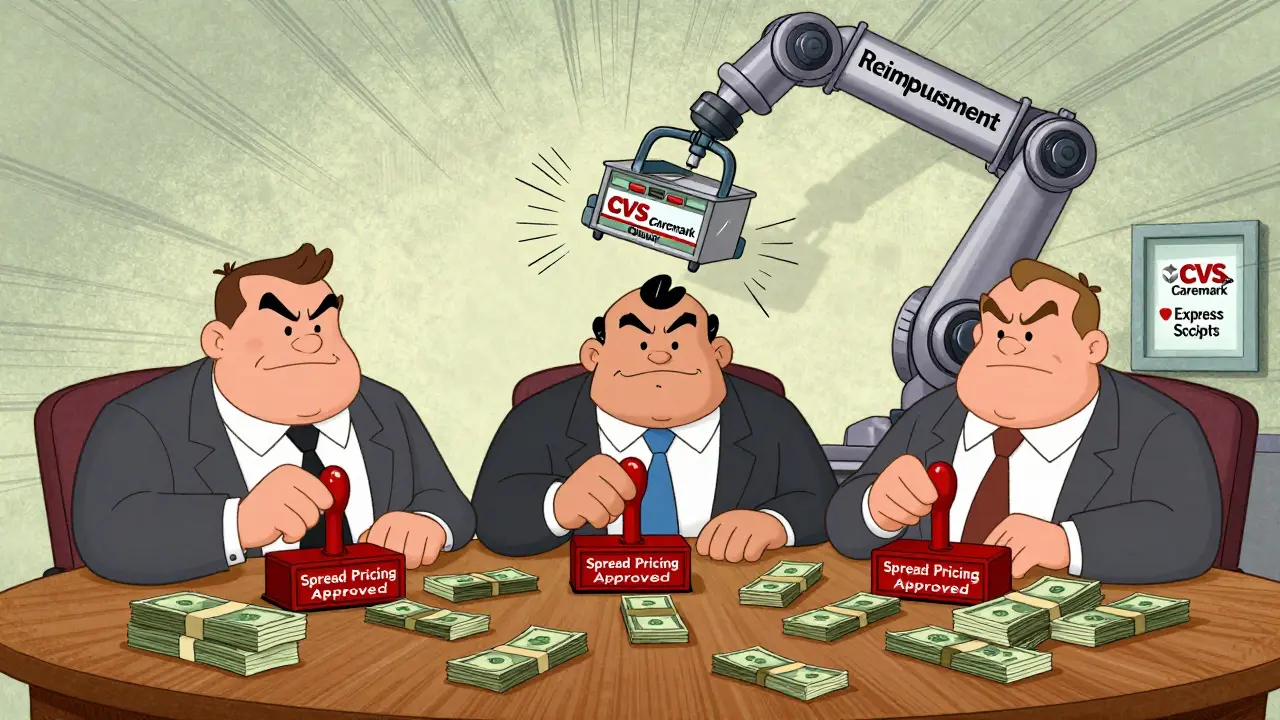

Three companies-OptumRx, CVS Caremark, and Express Scripts-control about 80% of the PBM market. That means nearly every insured American is caught in a pricing system run by a handful of firms. Their job? Negotiate with drug manufacturers for discounts, then set reimbursement rates for pharmacies. But here’s the twist: the price they tell your insurer they paid for the drug is often not the same as what they pay the pharmacy.

The mechanics behind the magic number

Here’s how it works in practice. PBMs create something called a Maximum Allowable Cost (MAC) list. This is a secret spreadsheet that says, "For this generic drug, we’ll reimburse your pharmacy up to $X." That number isn’t based on what the pharmacy actually paid for the drug. It’s based on an outdated formula using the Average Wholesale Price (AWP) or the National Average Drug Acquisition Cost (NADAC). Then they add a small dispensing fee-say $3 or $4-for the pharmacist’s time.

But the real trick is called spread pricing. Let’s say the pharmacy bought a bottle of generic metformin for $2.50. The PBM tells your insurer the drug costs $45. You pay your $10 copay. The PBM pays the pharmacy $7. The difference-$38-is kept by the PBM. That’s profit. And it’s hidden. No one sees it on your bill. Not you. Not your doctor. Not even your insurer unless they dig deep into contracts.

According to a 2024 analysis by Pharmacy Times, spread pricing from generic drugs alone generates $15.2 billion a year in undisclosed revenue. And 68% of that comes from the cheapest pills on the market-drugs like lisinopril, atorvastatin, and levothyroxine. The more volume a PBM controls, the more they profit from this gap.

Why you pay more than cash

It sounds backwards, but insured patients often pay more than people who pay cash. A 2023 Wall Street Journal investigation found that some cancer and multiple sclerosis generics cost insured patients over 10 times more than the cash price. A 2024 Consumer Reports survey of 2,300 people found 42% had paid more through insurance than they would have if they’d paid cash. One Reddit user wrote: "I paid $45 for my generic thyroid med. The cash price was $4. I cried in the parking lot."

This happens because your insurance plan’s formulary-the list of drugs your insurer covers-doesn’t always reflect real-world prices. PBMs design formularies to push pharmacies toward drugs they’ve negotiated the widest spread on. If a drug has a $30 spread, it gets prioritized. If it has a $2 spread, it gets buried under prior authorization requirements or higher copays.

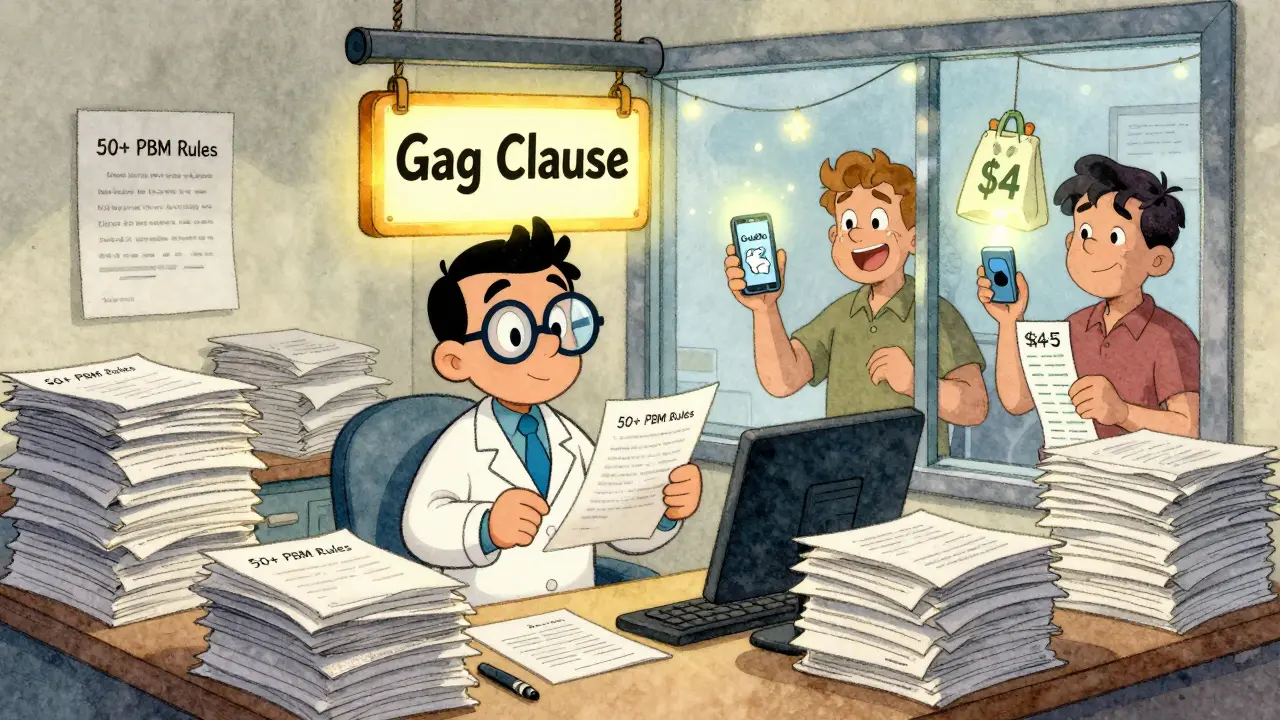

And then there are the gag clauses. In 92% of PBM contracts, pharmacists are legally barred from telling you that the cash price is lower. So you walk out thinking you’re getting a good deal. You’re not.

Who pays the real cost?

The pharmacy does. Independent pharmacies are getting crushed. Reimbursement rates keep dropping. In 2023, 63% of independent pharmacies reported PBMs clawing back money after a claim was already paid. That means you fill the prescription, get paid $7, then two weeks later, the PBM says, "Oops, we overpaid. Send us back $3."

Between 2018 and 2023, over 11,300 independent pharmacies closed. Why? Because the math doesn’t add up. One owner in Alabama told a reporter: "I spend 250 hours a year just trying to decode PBM contracts. I have to hire someone just to understand how much I’m getting paid."

And the cost isn’t just financial. Pharmacists now need specialized software to handle the 50+ different reimbursement rules from different PBMs. Setup costs? $12,500 per pharmacy. Training? Months. And changes come without notice. In 41% of cases, reimbursement rates shift overnight.

What’s changing? And what’s not

Pressure is building. In 2024, 42 states passed or are considering laws forcing PBMs to disclose spread pricing and MAC lists. The federal government isn’t far behind. President Biden’s September 2024 executive order bans spread pricing in Medicare and Medicaid, effective January 2026. The No Surprises Act already made it illegal to surprise patients with out-of-network bills. Now, the focus is turning to the hidden bills inside your insurance.

The 2025 Medicare Drug Price Negotiation Program is expanding to 20 drugs. While it only affects Medicare, it’s sending a signal: list prices aren’t sacred. And if Medicare can negotiate, why can’t private insurers? Experts estimate that if this model expanded to commercial plans, savings could hit $200-250 billion over ten years.

But the industry isn’t giving up. PhRMA and PBMs argue that these negotiations drive innovation. Yet the data tells a different story. A 2023 JAMA commentary pointed out: "Higher list prices mean bigger rebates, which means bigger profits for PBMs-and higher out-of-pocket costs for patients."

The truth? The system was never designed to save you money. It was designed to create layers of hidden revenue. And the people who pay the most? The ones who need the drugs the most.

What can you do?

Don’t assume your insurance is helping. Always ask the pharmacist: "What’s the cash price?" If it’s lower, pay cash. Use apps like GoodRx or SingleCare. They often show prices that beat your insurance copay. If your plan forces you to use a specific pharmacy, ask your employer to switch to a transparent plan. Only 12% of employer plans currently offer clear pricing.

And if you’re a pharmacy owner? You’re not alone. Join the National Community Pharmacists Association. Demand transparency. Push for state laws. The system is rigged-but it’s not unbreakable.

What’s next?

By 2027, McKinsey & Company predicts PBM spread pricing revenue will drop 25% due to regulation. But manufacturers may raise list prices to compensate. That means your copay might still go up-even if the PBM’s profit shrinks.

The real question isn’t how much a generic pill costs. It’s who gets to decide. And right now, the answer isn’t you. It isn’t your doctor. It’s a handful of corporations buried in contracts no one reads.

Why do I pay more for a generic drug with insurance than cash?

It’s because of spread pricing. Your insurer is charged a higher price by the Pharmacy Benefit Manager (PBM) than what the PBM pays the pharmacy. The difference is kept as profit. Meanwhile, your copay is based on that inflated price, not the real cost. So even though the drug costs $2 at the wholesaler, your copay might be $15. Meanwhile, someone paying cash might pay $4 because they’re seeing the true wholesale price.

Who are PBMs and why do they matter?

PBMs, or Pharmacy Benefit Managers, are companies that negotiate drug prices between insurers and pharmacies. They manage formularies, set reimbursement rates, and process claims. Three PBMs-OptumRx, CVS Caremark, and Express Scripts-control 80% of the market. They decide which drugs are covered, how much pharmacies get paid, and how much you pay at the counter. Their profit comes from the gap between what they charge insurers and what they pay pharmacies, not from lowering drug costs.

Is spread pricing legal?

Yes, it’s currently legal for private insurers. But it’s being banned in federal programs like Medicare and Medicaid starting January 2026. Several states have already passed laws requiring PBMs to disclose spread pricing. The federal government is moving toward full transparency, but until then, it remains a hidden revenue stream for PBMs.

Why can’t pharmacists tell me the cash price?

Because 92% of PBM contracts include "gag clauses" that legally prevent pharmacists from informing patients about lower cash prices. These clauses were designed to keep patients from bypassing the insurance system. In 2020, the No Surprises Act banned gag clauses for out-of-network care, but enforcement for in-network drugs remains weak. Many pharmacists still fear legal action if they speak up.

How do PBMs affect drug availability?

PBMs control which drugs are on formularies. If a drug doesn’t offer a high enough spread, it gets pushed to higher tiers with bigger copays or denied coverage entirely. This means even if a generic is safe and effective, it might not be covered if the PBM can’t profit from it. This reduces patient access-not because of safety, but because of profit margins.

Can I avoid this system entirely?

Yes, but not easily. If you pay cash, use discount apps like GoodRx, or shop at pharmacies that don’t participate in PBM networks (some independent ones do), you can bypass it. Employers offering transparent, direct-pay pharmacy benefits are rare-only 12% of plans do this. Your best move: always ask for the cash price before using insurance.